Competition and Outsized Returns in VC

My take on how VCs think about competition, standing out from the crowd, and generating best-in-class returns

Competition has a massive impact on a venture investor’s ability to create outsized returns, as it influences 2 things every investor cares about:

Getting into a deal

Investing at an attractive price

Simply put, the more competition there is from other investors, the harder it is to get into a deal and/or invest at an attractive price.

Investors, therefore, focus a material amount of time and energy on reducing competition, or more directly, doing what they need to do to get into the best deals at the best prices.

In order of priority, investors tend to focus on #1 first, which makes sense. If an investor can’t get into a deal they want, the price doesn’t matter. But even getting into a deal has its nuances: not only do you want to get into a deal, you also probably want to invest and hit your targeted ownership or check size. So, you may have the option to participate…but it might not make sense to. For a fund of a particular size, there comes a point where an investment is just too small to make sense because it either wouldn’t be impactful at a fund level regardless of its return potential, perhaps it would require too much time or effort that might see more benefit accrue to other investors, or it would fly in the face of a communicated portfolio construction (X% ownership, Y deals, etc.).

Another layer of getting into a deal is considering whether an investor wants to get into a deal as a lead or as part of a syndicate. Lead investors typically invest the most capital in a round, and therefore own more of the company than other investors in the round, often with board seats, formal pro rata rights, or protective provisions. Syndicate investors are left to fight for whatever allocation is left after that, and are often forced with a “take-it-or-leave-it” valuation number/terms that the lead investor set. You can fight all you want to get into a round, but if you’re a syndicate investor and not comfortable with the price, you’re forced to stay on the sidelines. Syndicates also tend to get ‘massaged’ the most to make room for other strategic investors because founders tend to optimize for the smallest checks that an investor would settle for. This allows founders to have the most value-add folks around the table.

To actually achieve #1, the things VCs do to get into a competitive deal (i.e., win allocation in a round) may include leaning on:

Brand + Reputation:

For a founder, hanging the flag of a well-known venture fund is a strong signal to other investors that you’ve cleared filters from a well-known institution, that the company will probably have a strong capital partner if things get tough (more on this later), and that there could be a big outcome. Big venture funds need to return a lot of capital, and settling for anything less than a big outcome isn’t ideal. That ‘big swing’ mentality can resonate with the market.

A well-known brand is also leverage for a founder in hiring. Top talent tends to follow the smart and/or big money.

Venture investors, therefore, focus on building a brand that is recognized by founders at the stage where they focus their investments. Some VCs are very well known at the earliest stages, and others at the later stages. The more a venture investor can tout their brand, track record, smart people around the table, experience/expertise, and overall influence creating a great outcome at their stage/sector of focus, the better their brands will be.

Valuation

A nail that any potential lead investor can hammer is valuation. This is a big variable for a founder, and although some may be turned off by a super-aggressive valuation, we simply didn’t see that through the frothiness of ‘20 and ‘21. Smaller and/or lesser-known investors may lean on valuation more heavily since those firms may not have the brand premium to win a deal. I won’t rehash the frothy valuation environment/correction summary here (same with the increasingly large round sizes at those valuations), but suffice it to say that investors have been very aggressive in the past…as of this writing in ‘23, that is no longer the case.

Speed and Efficiency

Similar to valuation, this is also a hammer every investor can nail: “I can close in a day and it’ll be the smoothest and least painful process you’ll ever see”.

Speed and efficiency can be a huge value for an investor who sees a deal first. Investors don’t want the deals they like to be shopped around, so moving really fast can get their foot in the door and save a founder time and cycles. I see this more often in the (really) early stages, where founders might be leaning more into a SAFE or convertible note that doesn’t require a formal lead, and there’s less certainty around how much capital can be raised. Twitter VCs, angels, and some hustle-focused solo-GPs are really good at moving quickly to get deals done.

Note that the pace of deals can often be inversely correlated with investor diligence: faster deals, less diligence. One can argue that the bar for VCs in ‘20 and ‘21 was much lower due in part to the speed at which they were required to invest and capital they were pushing into the market.

Value-add contributions:

I’ve observed that founders appreciate surrounding themselves with investors that they like and that can help create real value. Value creation can come in a variety of forms: board expertise, hiring, access to customer decision-makers, intros across an industry, or strategic advisory, for example, and an investor will tailor their pitch to a founder to focus on the specific things that they think they can deliver in a more meaningful way than others.

Being a strong capital partner:

Startups don’t always follow a consistent, up-and-to-the-right path, and strong, deep-pocketed investors can help immensely in a time of need. A small fund or one that doesn’t have a meaningful amount of reserves relative to a round size, capital needs, and traction, can be put in a challenging place if things don’t go right: founders often rely on their lead investors for continued support, and if they can’t get that, it’s a tough pill for other investors to swallow to continue to invest, or to be a new investor. In the market we’re currently in, having strong capital partners can be the difference between surviving and shutting down.

Secondary

A way for syndicate investors to invest is to create their own opportunity through a secondary purchase. This typically involves investors buying founder or early employee shares but could also include earlier investors who want to sell or take some chips off the table. Until recently, investors were happy to buy founder or early employee shares, often common shares at the price of preferred.

The talk track for an investor that wanted to go this route was something like: “Hi founder – if you or others want to take chips off the table, I’d love to buy the shares. Your existing investors should be ok with this because there’s no impact on the round – the ownership of the preferred investors remains the same – and the shares you own are still material to keep you motivated to ride this thing out long-term. Whattya say?”. Win for a founder (cash), win for the syndicate investor (allocation in the round, albeit potentially with common), and win for the formal round investors (their ownership stays the same)! There are some clear issues here, though…investors watching founders take millions of dollars off the table when there isn’t a clear reason to (say, a home purchase or a life event) can be a clear cause for concern.

Once you’ve gotten into a deal, you’re over the first big hurdle. Now comes the tough part.

Competition and Price

Competition and price are correlated – highly competitive deals tend to be the most expensive, and those without competition tend to be priced the most favorably – so it’s natural that it’s incredibly hard to get into a highly competitive deal AND come in at a low entry price. If a founder has cheaper capital where they’re going to take less dilution, the impact could be millions (or tens of millions) of dollars for them personally based on the exit size. Going back to brands, the Sequoia’s or a16z’s of the world may be able to pull a trump card and invest at a lower price than others because of their brand premium and aforementioned advantages, but many of us cannot.

So, what’s an investor to do? Just take the market price, or, at a minimum, pay up for every deal? Jeff Jordan, an OG in marketplaces and partner at a16z with an unparalleled track record operating and/or investing in companies such as eBay, Airbnb, Pinterest, Instacart, Affirm, Fanatics, OfferUp, Cadre, Lime, Wealthfront, OpenTable, PayPal (yeah, not a bad run.), is on record as saying that he usually hasn’t regretted paying up for a deal, but has been punished when he tries to invest in deals without any other interest. To me, Jeff’s feedback indicates that the venture market either 1) has group think or 2) is pretty efficient in spotting companies that can have meaningful venture returns. I suspect it’s actually both of those. At the end of the day, if you pay up for deals that work out, all sins are forgiven. But those deals that work out…really need to work out to see the outsized returns you need at a portfolio level. Portfolio construction has a big say in that (check size, ownership, investment size relative to fund size, etc.). Some funds recognize this and will often ‘chase’ deals led by the big brand name firms in hopes of ‘riding their coattails’ (or so we’ve observed with some of the smaller and/or regional investors across the country).

If you’re a venture investor and you follow the herd to invest in the hot spaces, you’re more likely to pay a premium as buy-in for the hype that drives more competition for deals, frothier return expectations, and a collective belief in a market that might not exist yet. As noted, if it turns out that you’re right, it’s generally a good outcome. But your entry point is slammed because you came in really high, which compresses your return. This can be an ok place to play, but it reduces the likelihood of a grand slam that creates the power-law returns that venture investors hope for. Some companies really will justify high entry points for investors over the long term. But the higher an entry price you pay, the smaller your margin for any error is.

It’s also worth noting - and a critical point to note - that when I’m referring to valuations, I’m really referring to multiples that investors are willing to pay. When competition is fierce and price goes up, it implies that an investor is willing to pay a higher multiple of ARR/GMV/whatever the company is getting valued on than other investors. Maybe an investor believes that the outcome will be way bigger than other investors, so the numbers pencil out. Maybe their cost of capital is lower and/or they’re willing to take a lower return for the risk. Maybe they just want to win the deal. Whatever the reason, the fact of the matter is that the valuation increases as a result.

Investors willing to pay more via multiple expansion is not a new concept. Per Seth Klarman in his seminal “Margin of Safety” (originally published in 1991), investors in a stock expect to profit in at least one of three possible ways:

From free cash flow generated by the business, which is eventually reflected in a higher share price or distributed as dividends

From an increase in the multiple that investors are willing to pay for the underlying business, as reflected in a higher share price

By narrowing the gap between share price and underlying business value (I take this to mean that the business is below cost, and eventually the market values it at par).

In the venture world, #1 is essentially off the table as there usually isn’t usually free cash flow to value.

#2 is absolutely on the table as it’s what we’ve seen play out over the last 2 years. Investors came in at multiples that made sense if either an investor further down the track was willing to pay a higher price (a Tulip mania, of sorts), or if the round might be big enough to allow a company to “skip a round” and grow into a higher valuation further down the track, even considering market compression. We watched sleepier companies and/or lower margin business models with higher capital intensity that raised rounds pre-COVID suddenly raising capital at massive upticks to their last rounds. Again, nothing had fundamentally changed about their businesses, but #2 took over. Early investors coming in at 3-5x annualized revenue didn’t have a lot to risk on the multiples side – the deals were very picked over, companies had been out raising for a long time, and multiples probably weren’t going to drop meaningfully more than at entry. Essentially, that leaves a call option from a multiple standpoint, where those early investors found themselves the beneficiary of multiple expansion that made their entry points look attractive to investors further down the track as long as cash burn didn’t kill the company. It's the ideal scenario for an earlier investor in that they bought prior to broader market awareness or ahead of improved operational performance that subsequently drives prices up for others and creates an outsized return for a fund.

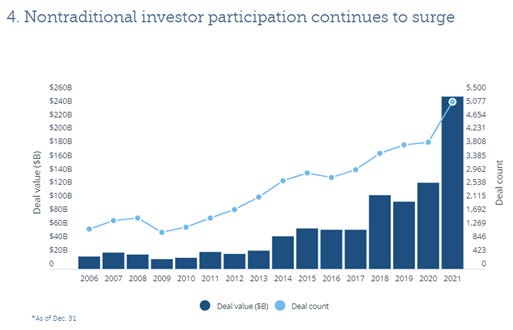

The problem with #2 is that multiples are driven by the market, not the operations of the business. Therefore, a founder can’t control it. Founders CAN control their business – the inputs and outputs of their business eventually produces a metric that investors assess and drop that multiple on top of, be it ARR or NOI or EBITDA. But nobody can control the market, and in an environment that was flush with cash and had an insatiable appetite for growth stocks, multiples exploded. It wasn’t that the businesses were becoming more profitable or growing greater ARR bases…it was more like $500K of ARR (with good growth!) * a 100x multiple. In the situations where investors were pre-empting rounds, it felt a lot like kicking the valuation can down the road and expecting the next investor to pay up and make the deal look good. Or you could point to the frothy public markets and assume $5B outcomes across the board. To highlight this, at the peak of the market in ‘20-’21, many public market investors were dropping into the late-stage private markets because they were seeing an arbitrage between the private and public markets. Public market investors were rewarding growth stocks handsomely, but there just weren’t enough of them to meet investor demand. Enter SPACs and the private investors plowing dollars in to hit the release valves of the public markets, and you get a huge volume of non-traditional investors playing in the venture game. The statistics on this are incredible: $329B was invested in 2021, and ‘non-traditional’ investors - hedge funds, crossovers, private equity, sovereign wealth, and mutual funds – accounted for $253B of it (77%)!

In that environment, I can’t blame founders for taking the cheap money and managing their business in a way that the market rewarded. Growth was rewarded at almost any cost. We’re learning now, though, that the blast radius for a founder to take on capital at an immensely frothy valuation will impact hiring, complicate capital raising, and place even more pressure on the business to grow.

Then there’s #3, which essentially says that an investor come in at a price below market. This is equivalent to saying that you’re a non-consensus investor in that you believe something is worth more than the market thinks it is. Investing at a discount, if you will. In a segment with lower valuations, the math from a DCF says that there is either lower implied growth, free cash flow, terminal value, or higher competition that would eventually compete away attractive margins. As an investor, where in that equation do you disagree? And is it realistic in a venture environment, where return expectations are so high and driven by the 100x returns we’ve all read about, that there are discounted opportunities?

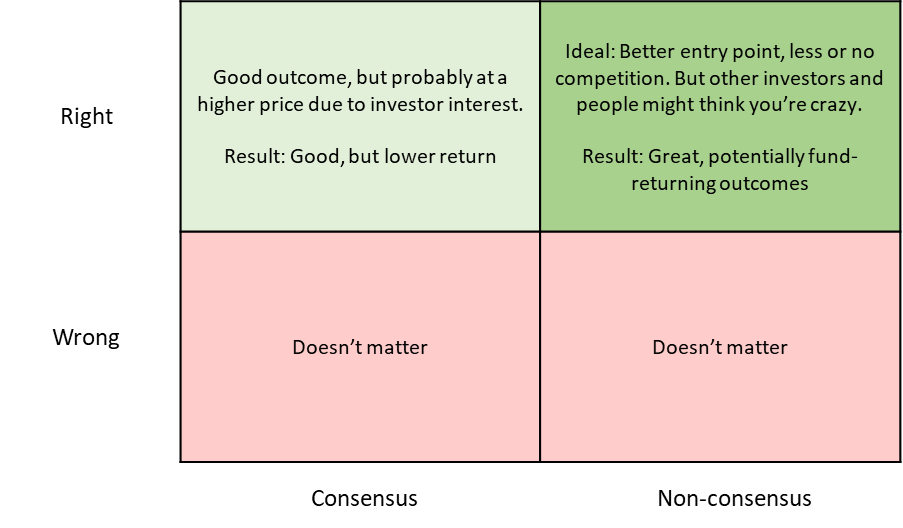

Fundamentally investing where you think the market has mispriced or not thinking through a strategy, market, team, or opportunity is tough, because it’s by definition non-consensus and ‘contrarian’. Contrarian investors often point to this strategy in making investments where others won’t, where others didn’t believe, or see, an opportunity, and where they made a boatload of money as a result. Their entry point was low and it was a grand slam. Making outsized returns could mean that you truly believed where others didn’t, and this allowed you to get in at a price below market, or below where the market should be pricing it. Perhaps it was a low-probability outcome, but the upside made it worth the investment on a risk-adjusted basis (see: Black Swan events).

Being a contrarian investor is often talked about as being a great thing – zig when others zag, and you can create something incredible. While there are instances where that is absolutely spot on, my feeling is that:

Those examples are filled with survivorship bias, and while we hear about the successes, we don’t hear enough about the losses.

This narrative can be a very dangerous one for a founder. We often hear stories about founders that ‘run through walls’ and that did everything they could in the face of everyone telling them that it couldn’t be done (e.g., the Airbnb founders selling "Obama O's" cereal around the Democratic National Convention). These stories can be inspirational to a founder: Never give up! Don’t let anyone tell you otherwise! Everyone is wrong but me! But…the danger is when a founder relies on this mentality and those few success stories in the face of feedback and guidance they’re likely receiving from some smart, experienced people. It’s tough as a VC to talk to founders when things seem so clearly to be trending in a stagnant or negative way, due to what seems to be obvious: competition is really stiff, differentiation among products isn’t meaningful, the market is maturing, switch costs are low, less capital is available to invest in these segments (…or whatever the reason). It’s really hard to be a successful founder, and the risks to build something from nothing, managing endless complexities, and withstanding the immense physical and mental tolls it takes are what I admire about any founder, successful or not. However, markets are pretty efficient, and investors are pretty smart. So, the feedback from both should be considered and balanced appropriately for founders and investors alike.

There are also stories that investors tell their LPs about how they came in at a great price, or ended up owning much more of a company for whatever reason. Again, the devil is in the details. If an investor is clearly making a contrarian move and think the market and/or other investors are wrong, that’s great and should be articulated as such. Perhaps they are a value investor and the company has cash flows available to them at a discount (usually not in VC opportunities), and the investor is happy to pounce. But I find it problematic when an investor uses that narrative to their investors when, in fact, the price was low because the company was actually shopped around a bunch, growth prospects were slow/low, or the market size wasn’t big, for example. There is a fundamental difference between having a low valuation and being ‘underpriced’, and representative of a great deal for an investor. The challenge for LPs is that they aren’t usually in the weeds and may not know one way or another what’s really happening. LPs care about returns – and if there are returns, usually questions aren’t asked. But returns over the long run remove the outliers, and expose the investors who have a long-term ability to generate returns vs those that may have timed the market well and/or hit a blind grand slam.

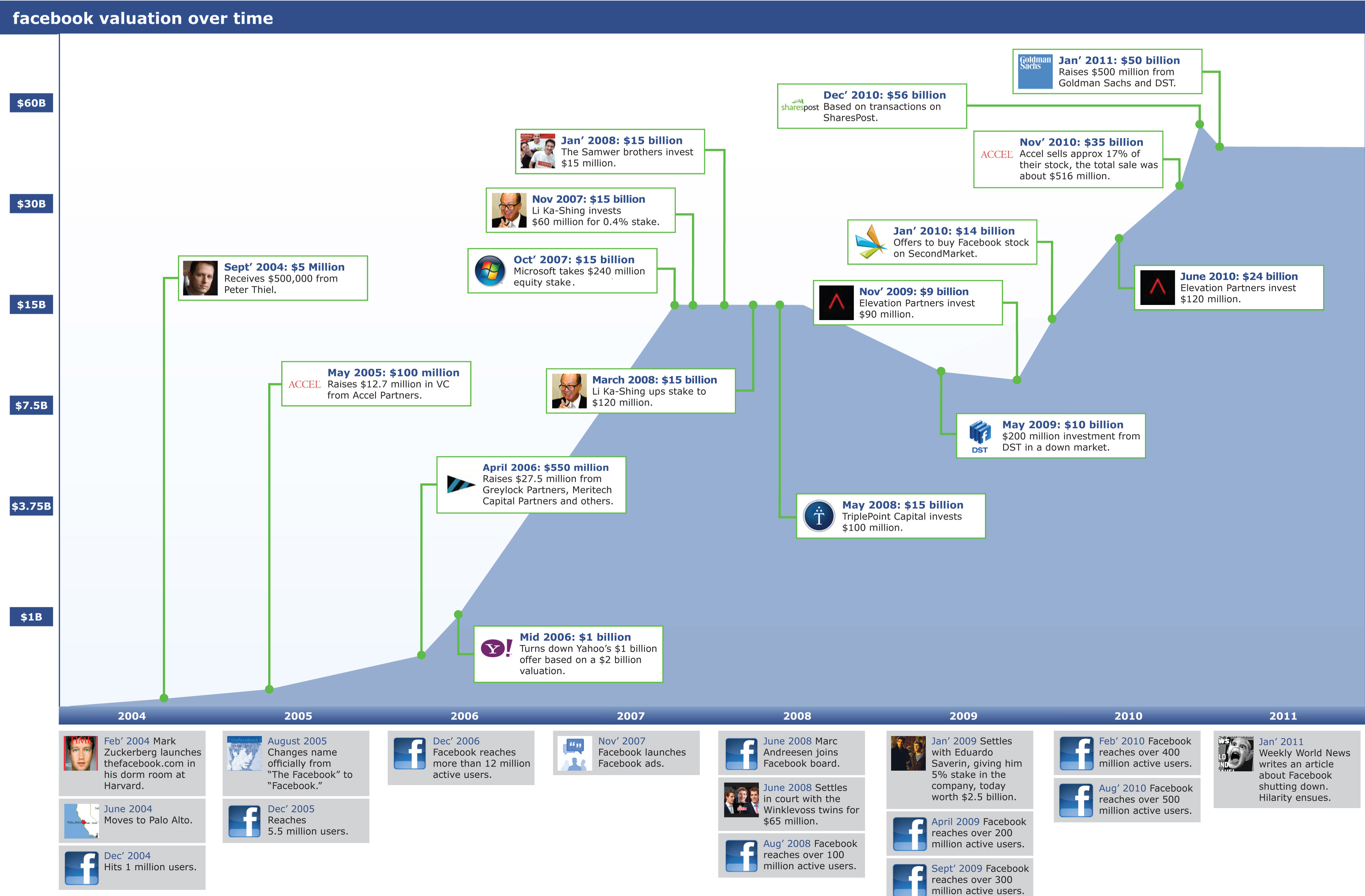

Another challenge with #3 is that it’s hard to say whether an investor came into a deal because it was a hot deal and right, and a big outcome, or non-consensus and right, and made a ton of money. Take Facebook for example. Facebook’s valuation across their rounds was:

Facebook was a hot deal. Everyone wanted in, and pretty much any VC who came in made a ton of money. Consensus + right. But how does that explain the massive outcome? Hindsight being 20/20 you can argue that EVERY round of Facebook funding was underpriced relative to the outcome. But at the time, nobody knew how big of a company it could be, whether the team would crack, or how influential social media could become. But it had the potential to get there, and occasionally a Facebook or a Coinbase will be the catalyst for a massive macro shift, be it social media or crypto.

So back to the original question – is it possible, in as connected and transparent a world we’re living in – where information, relationships, and startups are almost immediately exposed to seemingly every investor out there – to invest in attractive venture opportunities at a discount?

I believe it is possible, but there are conditions and considerations:

I think you need to be investing where others aren’t, or where investors don’t understand the complete picture.

Look at where we are today with SaaS investing: there are now industry benchmarks, efficiency numbers, and models that come along with any SaaS company across funding stages. Investors have a much more accurate way to benchmark relative and absolute performance and price that into deals. I’d venture to say that across the board, SaaS valuations are in a tighter band today than they have been over the years because of the broader understanding and maturation of the market.

Therefore, if there’s a new market or opportunity, there will probably be more mispriced opportunities there than in an established segment with a lot of data, people, and historicals to rely on (hello, AI!).

In the PE and/or buyout world, there could be opportunities to find companies in ‘sleepy’ industries where an owner wants to sell. The opportunity may not be shopped around as actively – or in a digital or streamlined way – as what we see in venture. Startup founders, though, are really good at leveraging their networks to share information about who they are, what they’re doing, and their fundraising plans, to reach a large audience quickly. Suffice it to say that I don’t think there are as many 65-year-old plumbers leveraging their Twitter followers, LinkedIn, Discord, or Telegram networks as we see in most younger startup founders.

Manufacture the outcome

Depending on when you invest, there are some benchmarks for what is expected to be done at each round of funding for a startup. Series A? $1M ARR for a SaaS business. Seed? Product and maybe a bit of revenue to help focus what to build and where to lean in. Pre-seed? A team, a product, or a firm grasp on product. Depending on when you invest, if you can manufacture the outcome at your respective investment stage, you’ve helped a founder/startup get to their next phase of financing and company growth. That’s big value and a successful playbook for a VC, but it’s tough to do given the time and resource intensity it can require across a portfolio.

Investing first can be an advantage

As previously noted, if you’re the first to act, an investor can benefit from reducing the number of eyeballs and firms in the mix. This is more relevant in the earliest stages, where a founder or team may not have a product or service that’s hit the market yet. Once something is ‘in the wild’, investors are quite efficient in finding companies. Once companies start trying to be seen they’re trying to reach the broader market (venture investors included), and it isn’t hard for venture investors to find them, as they’re on the lookout for precisely these types of companies.

This is somewhat counterintuitive, in that founders want to get a fair valuation for their company, which implies shopping an opportunity around a bit. That increases competition and could drive up prices. However, in the early stages (pre-seed, particularly), networks tend to be more limited to the founder vs a broader team that can all be leveraged to make intros and share deals.

Be the ‘smart money’, and know where an opportunity is ahead of time

If you become a pro in an investing segment, you should be able to spot the discounts and where things are overpriced. You know what cost structures should look like, what distribution works and doesn’t work, competition in the space, people and networks to tap, customers you think could be interested, maybe even some potential employees that would be a good fit. This allows an investor to filter the noise, avoid the Ls and focus on the value.

Focus on the strategic positioning, not on a spreadsheet

Massive venture outcomes are created by companies that often have common strategic structures and strengths. Network effects are usually the first and most prominent example because network effects are responsible for a company’s ability to create more value as they get larger. The larger the network effects, the easier it is to defend. That’s the dream – more value, easier, and at greater scale – that can unlock huge value as an investor. Other Clay Christensen and/or ‘7 Powers’ principles take charge here as well.

The point of strategic positioning is really to focus on competition and the barriers/moats a firm can put in place. The bigger, stronger, and longer lasting those moats and competitive advantages exist, the more money a company and investor will make. Competition kills companies and returns.

Know what game you’re playing

Fund strategy dictates everything: the types of LPs a manager targets, the types of companies they invest in, the capital they deploy and reserve…everything. You’re more likely to win the game if you know what you’re playing.

A fund may be in the AUM game (more AUM = more fees, and either more deal velocity or larger checks), generalist vs focused on a specific industry (healthcare, construction, etc.), small / mid / large fund, active with portfolio companies vs passive, corporate/CVC vs not, etc.

It’s important to know what game you’re playing so that you know what rules to follow, and when to break them. The trick is knowing when to do either/both.

So how do you know if you’re getting in at a below-market price vs an accurately reflected low valuation?

Longtime investor Howard Marks provided some very interesting commentary and perspective on finding value in a world where information is much more freely available, open, and generally lacks asymmetry relative to a few decades ago. As a result, he stated “…successful investing has to be more about superior judgments concerning (a) qualitative, non-computable factors and (b) how things are likely to unfold in the future.” since investors have more or less complete information now.

I can’t think of many easy ways to learn to make superior judgments about qualitative, non-computable factors and/or how things are likely to unfold in the future. It takes experience and a keen sense of risk and return to assess investment opportunities. That said, I find that asking a lot of questions can be helpful here in order to get a more accurate picture of pricing and valuation:

Does this company pass our ‘strategic filters’ that we have in place to identify those companies with characteristics that create bigger competitive advantages over time?

If yes, I get more excited about the opportunity and the value that the company can create over time.

How long has this company been raising? If it’s been a while, why haven’t they been able to raise capital yet, as they’ve been talking to some seemingly smart investors?

At a high level, we think there are some really smart, sophisticated investors out there, and if they’re all passing, it puts our guard up.

Why are we seeing this deal vs others?

If we see a biotech deal, something is off. We shouldn’t be getting that look, and it would seem as though everyone else said no.

Do we know what the market size currently is, and where it could be? If we value the company based on the current market, what does that imply? If a company can ‘expand’ their market, what value would that create?

We might know the current and future markets better than other investors

What do we know about this space that others don’t? Is there something that investors likely believe that we don’t? How does that factor into the valuation?

In the pre-seed: what do we know about the founder that would indicate they can get this company built? Impressive experience? Prior founder? What were the outcomes?

Is the company capital-intensive? Low margin/high margin? What’s the return on that cash?

If answers to the above point to a non-competitive deal or something that we believe we have a knowledge, experience, or network advantage on, we can get a better sense for true valuation and where we might be able to enter.

Numbers Must Pencil at the Fund Level

The above commentary generally focuses on deal-level dynamics, but fund managers are assessed by many investors based on their performance at a fund level relative to peers. So all of those individual battles that an investor must win to get into deals at attractive prices add up to how the war at the portfolio level is fought (and won/lost).

An essay by Bryce Roberts here sums up some of the challenges of making fund-level math work:

We have now reached a point in the startup ecosystem where for large VC funds, a startup achieving a billion-dollar outcome is meaningless. To hit a 3–5x return for a fund, a venture partnership is looking to partner with startups that can go public at north of $50B dollars. In the entire universe of public technology companies, there are only 48 public tech companies that are valued at over $50B. To hit this $50B hurdle, entrepreneurs take on more and more risk to try and achieve larger and larger outcomes.

These economics are an example of how an investor may not do a deal because its outcome will not move the needle for the fund. It also highlights how hard it is to return a $1B+ fund. If you’re an LP in that fund, you’re forced to think long and hard about the enormous scale that your exits require. I think the dynamics around fund returns are interesting and will continue to write about them, particularly around fund size. If a $50m fund returns $200m, it’s a solid outcome, even though the absolute dollar amounts pale in comparison to the sport that mega-funds play. BUT…the IRR and cash-on-cash returns are very likely better than some of the biggest funds (and names) out there. Another layer of complexity is that the biggest pensions, endowments, sovereign wealth funds, and family offices generally avoid the small funds because they aren’t big enough to move THEIR needles. Hence the small VCs court the smaller LPs, which opens another set of questions around the incentives for those fund managers, future performance relative to size, and competition.

Wrapping up:

I think it’s important to note that “outsized” returns are relative: generating outsized returns means that an investor wants to generate superior returns when compared to everyone else. So, by definition, a fund investor cannot do what everyone else is doing, or look like the other funds, or their returns will be just like everyone else’s. If the tide for a specific vintage, size, stage, or business model rises, all ships rise with it. That isn’t enough, though: the best fund managers are those that outperform others within the same segment. Those managers tend to make the most money for their LPs, create the strongest brands, and create a sourcing and value-add flywheel that creates successful and enduring firms.

A topic for another day is how an investor can create outsized returns on capital relative to risk (i.e. how do you control downside risk and have the ever-elusive uncapped/asymmetric upside, where a small investment can snowball into a massive outcome with option value and controllable growth levers along the way). These can be more creative and growth-focused strategies such as buying a company as a seed for a more robust and scalable platform in the same space, incubating companies with founders or operators that have unique insights or experiences, or simply identifying an opportunity/strategy before anyone else, so there is no competition.

Zooming in a bit at a deal level, competition drives ‘deal heat’ that bids prices up and makes things move fast. Investors will always have to deal with that, and as a result, spend a lot of their resources to compete and win deals. However, there are ways to create value by investing in companies where there isn’t as much competition, and therefore more reasonable valuations. But the trick for an investor is to understand WHY a deal is priced the way it is and to assess whether a valuation is low but accurate vs fundamentally mispriced and a bigger opportunity. These opportunities were fewer and farther between in the peak valuation environment, but could be more relevant in the current market as non-traditional investor dollars are sucked out of the system and pumped into other asset classes. It’ll be those managers with dry powder who view the world differently and are right that will ultimately win deals and generate the outsized returns we’re all hoping to deliver.